Best Graph I Have Seen Showing The Impact of Covid19 on CRE Values

Best Graph I Have Seen Showing The Impact of Covid19 on CRE Values

Bubble Watch: Coronavirus slashes commercial property values 24%

By JONATHAN LANSNER | jlansner@scng.com | Orange County Register

PUBLISHED: March 17, 2020 at 11:44 a.m. | UPDATED: March 17, 2020

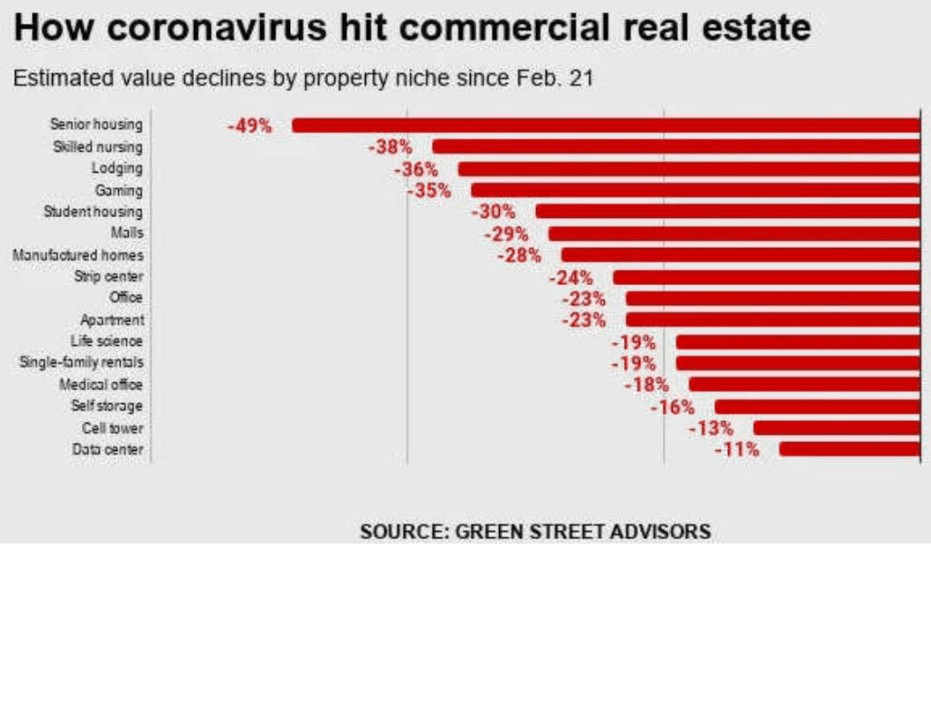

Buzz: Commercial property values are off an estimated 24% since Feb. 21. It’s another example of fallout from coronavirus fears and preventative measures that have upended the economy and raised huge questions about a key cog in the property investment game: tenants’ ability to pay the rent. Source: Green Street Advisors

The Trend

Commercial real estate looked like a great investment a month ago, even after a powerful upswing from the carnage of the Great Recession a decade ago.

Red-hot demand for real estate pushed up values in all sectors. And even the few weaker niches had built-in real estate worth — owners could sell at a premium for other uses.

The coronavirus, seemingly overnight, throttled many businesses that occupy real estate or drastically changed the economics in others. All of a sudden, giant, institutional real estate owners have two big questions: Can I collect the rents? And how can I pay back my mortgages?

In a report titled “Pencils Down,” the property gurus at Green Street in Newport Beach looked at stock market trading in commercial real estate investment trusts. What they saw was a 35% hammering of REIT share prices since COVID-19 hit the news. Green Street translated this walloping to a 24% drop in commercial property values. Yes, stock markets can overreact.

Ponder these slashed values by REIT segments. You can see what industries have become “essential” and which ones are either badly damaged or have quickly become risky.

The smallest losses were found in trusts specializing in data centers (off 11%) and cell towers (off 13%). The Internet and smartphones have grown in importance during this crisis. Think about it: If you lost your job you still need information, desktop or mobile.

The biggest losers? Real estate dedicated to caring for the elderly. Senior housing trust prices are off 49% and skilled nursing properties are down 38%. Increased medical risks, no less the loss of clients from a disease highly lethal to seniors, have walloped these shares.

Losses nearly as bad were found in industries practically empty these days: trusts owning hotels are down 36%; casino owners, down 35%; student housing, down 30%; and big shopping malls are down 29%.

In-between these extremes, you find real estate losses tied to daily necessities: Self-storage trusts are off 16%; medical offices, off 18%; single-family home rentals, down 19%; apartments, down 23%; strip shopping centers, down 24%, and manufactured homes, 25%.

And trusts who serve businesses were hit, too: Those owning life science facilities are down 19%; offices, down 23%; and warehouses and factories, off 28%.

The Dissection

Being a landlord seems simple. Acquire property, often with borrowed money. Find tenants. Collect rents in excess of expenses and operating costs. Reap that profit and hope for some asset appreciation, too. Let’s toss in some juicy tax breaks, to further sweeten the pot.

But what if your tenants can’t pay the rent? Or your banker won’t easily refinance your loans? Or potential buyers dry up and you’re left without an exit strategy?

All of a sudden, the business of being a landlord becomes very difficult. That’s commercial real estate today.

“It is impossible to peg where real estate asset values will ultimately settle,” Green Street wrote. “The tail risk associated with the COVID-19 spread has grown. Though the dramatic shift toward social distancing should help “flatten the curve,” the economic impact will be massive. Geopolitical ripple effects have materialized, such as a lower probability of a second term for President Trump and oil market turmoil. One can only guess which dominos will tumble next. Our crystal ball is as cloudy as ever.”

How bubbly?

On a scale of zero bubbles (no bubble here) to five bubbles (five-alarm warning) … FIVE BUBBLES! Yes, FIVE!

Look, the commercial property bubble has burst, even if it didn’t happen in an expected way.

Please don’t think that just because your real estate doesn’t trade in real-time stock markets that values aren’t damaged. Green Street estimates that bond market activity suggests commercial property values are off at least 15% in this same period.

Loss estimates aside, now comes the tricky part. Do we find corporate empathy in what’s perceived to be a short-run economic downturn, so maybe some asset depreciation is contained or reversed?

This scenario requires landlords to exercise some empathy toward virus-strapped tenants while lenders act in similar fashion toward the property owners they gave mortgages to.

Or does it become an ugly everyone-for-themselves? Will evictions and foreclosures become rampant, especially if the economic fallout is longer and deeper than originally feared? Then deep-discount fire sales of distressed property become the norm.

Answering these question will require more than a sharp pencil. It requires a psychology degree.